First things first, number-crunching, insights-gathering and models-building are not new to the insurance industry. Actuaries have always been at the heart of the practice and played a key role in helping insurers make sense of the data gathered since the 18th century and make decisions when it comes to their risk tolerance and appetite.

But the rise of technology solutions has brought about the gush of data from numerous sources and every other industry is seeing the emergence of a new profession: the data scientist. The work they do is so much alike to an actuary that the internet is so torn between the both.

Is the birth of data science the damn of actuary science?

Despite that said, the industry is pretty much in consensus that the actuary wouldn’t be made redundant but requires development in its role to fit the requirements of the changing world. Being an industry ladened with business processes, regulatory and accounting requirements, actuaries often have to undergo rigorous formal training and have ample experience to hold its ground in the insurance industry.

Like the insurance agent (aka the financial advisor or consultant now), the work of the actuary will evolve and innovate to bring about a more direct and meaningful impact on their potential customers – contrary to the common misconception that they’re seated hunched behind a computer at the back of the office, crunching numbers.

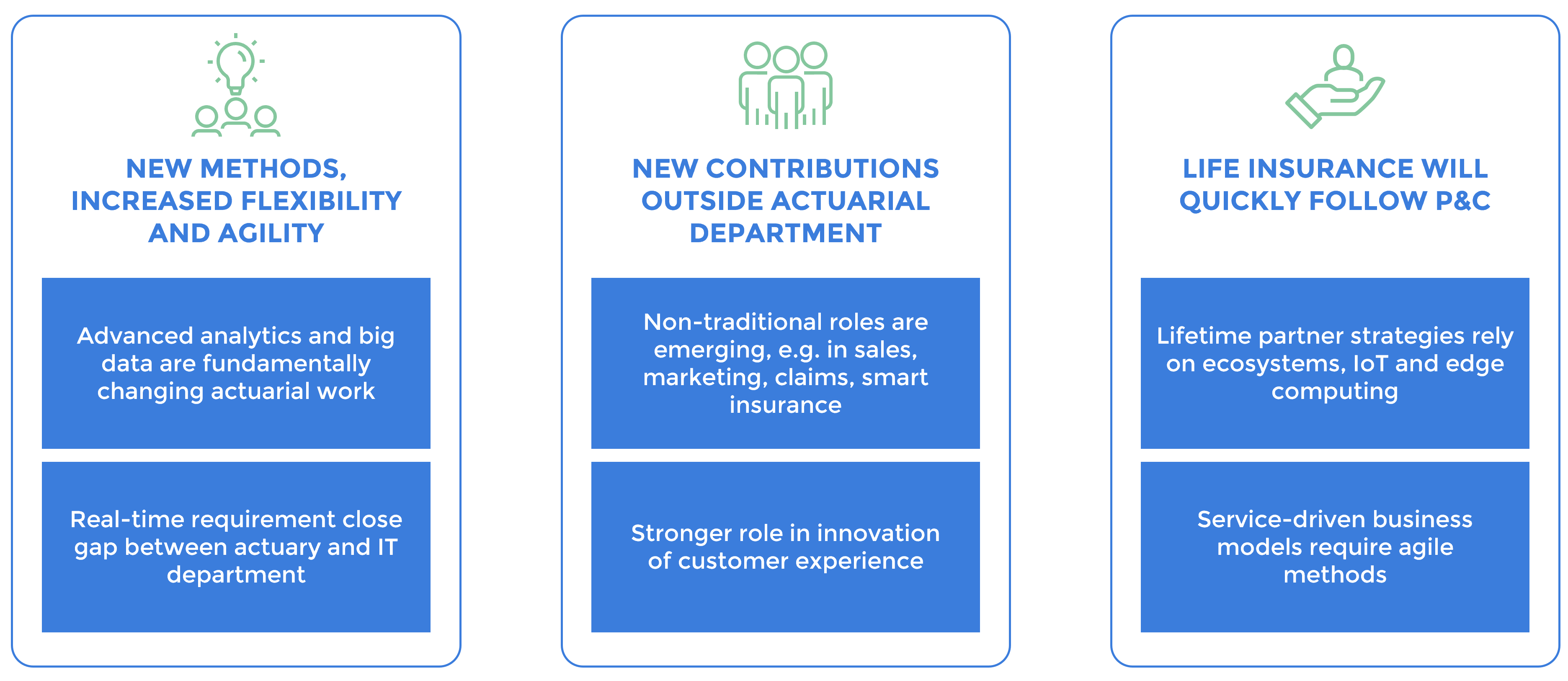

Forces shaping the “New Age actuary.” (Source: The evolving role of actuaries for insurance innovation, sas blogs, Sept 2020)

Beyond risk assessment that actuaries mostly deal with, in this article we want to make a case for data analytics in our industry. And how the impact of data has seeped into every other stage in the value chain, every other personnel in the insurance industry, and the role of insurers in today’s economy.

A new market research report by Meticulous Research highlights a number of insights on the state of data analytics in the global insurance market:

| Current (2020) | Forecast (by 2027) | |

| Global market size | USD 8.5 billion in 2020. | To reach USD 18.5 billion by 2027, at a CAGR of 12.2% during the forecast period of 2020 to 2027. |

| Insurance function | Pricing and risk management segment. | Customer management and personalization segment to record the highest CAGR during the forecast period. |

| Deployment type | Cloud over on-premise solutions. | Continued rise of the Cloud. |

| End user | Insurance companies. | Government agencies to record the highest CAGR over the forecast period. |

| Region(s) | North America, followed by Asia-Pacific, Europe, Latin America, and the Middle East & Africa. | Europe to record the highest CAGR during the forecast period. |

The aforementioned predictions are consistent across many market research reports. While it’s with no doubt that the ROI from deploying data analytics in the insurance value-chain will be plentiful. Yet, it can be painful to implement and integrate across the organization given the resistance to change – both on the fronts of legacy infrastructure and human skill sets needed.

For instance, this means transforming the actuarial role. Even within their traditional scope of work in pricing, valuation and regulatory reporting, the value that data-driven insights can bring is bountiful. Say in pricing insurance products, traditionally insurers have only used a few pricing bands (what they used to call a “one size fits all” model to pricing) and customers are evaluated depending on a few simple metrics. As we throw analytics into the picture, now you get:

Now that analytics as a tool or a means to a greater end has been covered, we want to move to the data pool where you use your tool to extract useful insights to your insurance business. And to explore the importance of tapping on unstructured data for the industry.

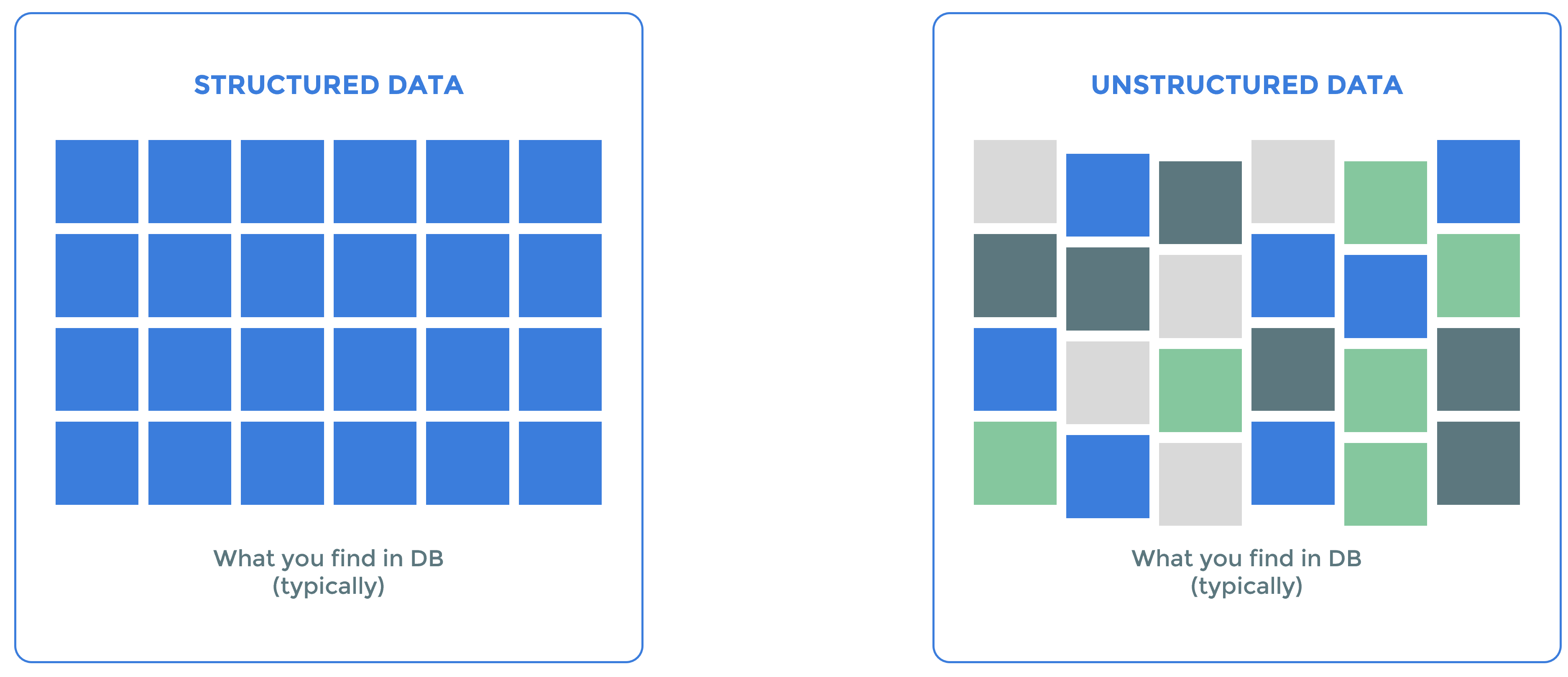

As much as 90% of the data out there is unstructured data. Unlike structured data, they don’t fit nicely into a box. Think of structured data like entries on a Google Form. You can easily generate them into columns and rows on the Excel spreadsheet.

Source: Unstructured Data vs Structured Data Explained with Real-life Examples, Yunee Ham, Jul 2020

For unstructured data, your potential customers are spontaneously generating these data as they’re online. Some examples of unstructured data are like Facebook comments, Tweets, email messages, instant messages, and audio or video files.

That said, for us, it’s more challenging to analyse and not as easily searchable. This also means that this type of data is not tapped into enough yet for the insurance industry. Ever thanks to advances in AI and ML, insurers can now tap into insights specifically from unstructured data.

Having a lot of data is good news, but not ideal when not all of these comes in useful for insurers. You want to be able to make use of a selected portion of the vast data pool to hone your existing product offerings and come up with new ones to serve untapped markets.

And getting the right data is facilitated by forming digital insurance partnerships to capture specific and diverse types of data of your targeted markets.

Digital insurance partnerships can vary from:

Consider telematics data from ride-sharing companies for auto insurance, or our health data gathered from wearables and mHealth devices for health insurance. Who better to get it from than your partners who service these markets directly?

On new product offerings, McKinsey & Company puts forward the multiple roles that insurers play in a particular ecosystem. In the example of the personal-mobility ecosystem, there is a range of opportunities for insurers to expand into areas such as vehicle purchase and maintenance management, ride-sharing, carpooling, traffic management, vehicle connectivity, and parking – where there is something for risk management and prevention in every one of these areas.

Traditionally, B2B2C insurance distribution has always been done via agents and your face-to-face interaction and relationship with your insurance agent have been at the hallmark of the distribution model.

Post-COVID-19 in a world where consumers are better informed, hyper-personalised and have higher expectations in the products and services, we need to consider how to redefine insurance distribution in the remote world. Agents will be deployed to provide more meaningful, real-time customer service that’s enabled by digital tools.

There will be more product offerings catering to the diverse needs of every individual consumer. The value of the product, its distribution and the service (or self-service) that follows after will be centred around the consumer, than it being limited to what the insurer can do on its individual platform.

It’s an ultimate win-win situation for both the insurer and the partner. Expanding distribution partnerships could help insurers to reach out to potential customers more effectively on insurance products that matter to them through their distribution partner. For the partner, this means a commission revenue earned on their end. Their value proposition would also expand given that the customer’s purchase extends after-sales.