Emerging or developed markets-alike, the demise of an one-size-fits-all approach for both banks and insurers. How should insurers reach these emerging markets at scale within the most practical means?

What does it mean for insurers to go digital? Many times, it’s often supplementary than necessary. The impetus of going digital tends to revolve around staying ahead of competition, keeping up with the rising digital native consumers, and improving customer satisfaction – adding value to existing products and services. But what if… the only way is digital?

Think about the traditional way we buy insurance: Multiple visits to the office, long turnaround times, reams of paperwork and occasionally, the human errors that come with these. And that’s only the purchase part of it! Don’t forget about claims submission and receipt… Let us consider customers who live far away from town or/and do not have the time to do all of the aforementioned within office hours, most would not have made it past the customer onboarding process.

That said, the potential of using insurtech to deliver insurance to the emerging market is far-reaching, and there are takeaways to gather from what our banking counterparts have done in these areas like how it is different from developed markets. We explore how digitalization can become a mediator for insurers to tap on the emerging market.

Formal financial institutions have often failed far-reaching rural populations for various reasons like inconvenient location and the incompatibility of one-size-fits-all financial products. Emerging or developed markets-alike, the demise of an one-size-fits-all approach for both banks and insurers is a key takeaway here.

Back to the point, this financial gap has led to the rise of leveraging upon mobile services to provide access to financial services in the emerging market. As McKinsey & Company says, mobile money is “much more than a “use case” … a lifeline, bringing the benefits of financial services to those who currently lack access.”

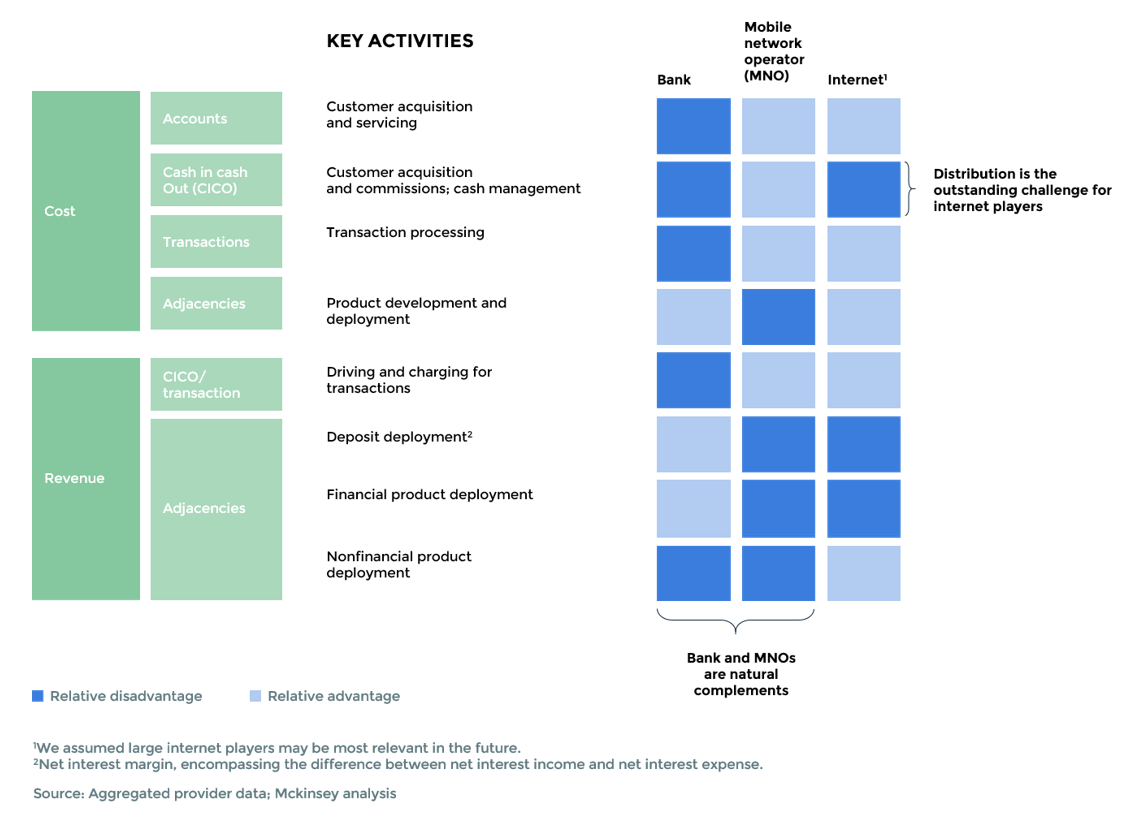

When it comes to scaling up the financial services in the emerging market, the mobile network operator and the Internet are at a better position to provide financial services to this untapped market than the bank:

Also, it’d be far-fetched for us to say that the insurance market is saturated. We have a long way to go when it comes to closing the protection gap between insured losses and actual economic losses. According to Swiss Re, the global insurance protection gap is estimated to reach a “new high” of $1.24 trillion in 2020 and in emerging markets, insurance and savings still meet less than 10% of the population’s protection needs.

Particularly in the life insurance portfolio, emerging market premiums are expected to outpace developed market premiums. Some drivers of growth include:

Traditional distribution channels like the use of brokers, agents and even bancassurance (selling insurance through banks) are capital-intensive on staff expertise and infrastructural investments. Aforementioned that these channels are geographically limited to urbanized areas and are expensive to set up in the constantly evolving and growing rural areas.

Given the low penetration of insurance in emerging markets, there is often low consumer awareness and trust with insurance products. That said, both the products and platforms where they are being distributed need to be easy to understand and easy to use such that they engender consumer trust and are cost-effective to provide.

How to reach these markets at scale within the most practical means? By making distribution more efficient and effective in its outreach, the cost of the product (premiums) can be lowered to achieve economies of scale. This can be done by embedding insurance within contact points frequented by potential customers. Some of these include the local shops, minimarts, telcos, microfinance institutions and farmer cooperatives.

Given the high smartphone penetration in the emerging markets, the digital channels can be leveraged upon to connect and serve these potential customers. With 75% of its customers now accessing insurance for the first time, BIMA, a startup that provides life and health insurance, has leveraged on both partnerships with leading telecom players and the increasing penetration of mobile phones across Africa and Asia to reach traditionally underserved consumers – by embedding health microinsurance within the mobile phone ecosystem.

| Developed Markets | Emerging Markets |

| ● Entry point tends to be auto, renters and property insurance.

● Health and life insurance market is saturated. ● Opportunities in coverage gaps in the market (e.g. telco-specific insurance, pay-per-mile, on-demand insurance, and bundling/unbundling of the product). ● Consumers are more informed, savvy and autonomous today. ● Consumers have higher expectations of the core insurance offering (e.g. Insurers to offer non-insurance products that add value to the core product – financial planning, home security, etc.). |

● Entry point is more likely life and health insurance for lower-income individuals.

● Higher demand to cover natural catastrophes. ● Lack of formal institutional infrastructure to reach a critical mass. ● Consumers have a low purchasing power and limited payment options. ● Microinsurance model requires hyper-targeted offerings to meet precise customer needs, while reflecting realities of their limited spending power. ● Opportunities in coverage gaps in the market (e.g. insurance to cover crop damage). |

Some differences between insuring developed markets versus emerging markets

What we see across insuring developed and emerging markets is the greater diversity within the respective markets. No one consumer is alike to one another and thankfully today, we have a pool of technology tools that we can use to harness data that will allow insurers to better understand their customers.

The low penetration of insurance in the emerging market is a testament to the failure of a one-size-fits-all-approach. The more customized the business model, the better the overall outcome. As illustrated In the BIMA example, none of the incumbent insurers was able to tackle as well as this Swedish microinsurer who went down to the nitty-gritty details of their potential customers.